It’s no secret that, following the financial crisis, small and mid-sized business (SMB) owners have been long on complaints and short on love for their banks.

While lending restrictions seem to be easing somewhat recently, SMBs have struggled mightily in terms of getting approved for business loans. But it’s not just the difficulty of securing lines of credit or business loans that have SMBs unhappy. Business customers have also been vocal in complaining about the lack of leading-edge products and digital solutions available to them from their primary banking partners.

According to the findings of our recent Performance Against Customer Expectations (PACE) Report, the situation may well be approaching a tipping point that could lead to significant defections of SMB accounts for their primary banking providers.

In the 2017 PACE report, we surveyed nearly 500 U.S. businesses with revenues up to $500 million and asked how they felt their banks were meeting their expectations. Specifically, the study showed that 14 percent of SMBs switched banks in the past 12 months and an even bigger percentage of these businesses are considering moving to a different primary banking provider in the next year.

It's not just about fees and denied loans

Interestingly, the 2017 PACE report revealed that not offering leading-edge products and digital solutions plays a key factor in SMB dissatisfaction with their banking providers. In fact, 48% of SMBS that reported that they are considering switched cited "product/service offering lacking" as a main factor.

The desire for modern digital banking options among SMB owners isn't surprising. After all, these businesses are being run more commonly by millennials and are serving the needs of millennial customers, who are accustomed to running their lives via digital means. Findings show that across all business revenue segments, 68 percent of SMB customers' banking interactions are online or mobile.

According to PACE, while the use of mobile banking is rising across all age segments, mobile banking penetration is highest among younger businesses. Indeed, mobile banking can be considered as table stakes for banks wishing to serve this segment.

Lack of leading-edge apps also appears to be playing a factor in SMB dissatisfaction with their banking relationships. The 2017 PACE report revealed that 37 percent of SMBs surveyed use nonbank financial apps to pay vendors and suppliers. It's even higher - at 49 percent - for businesses with more than $25 million in revenue.

Who will win the battle for SMB customers?

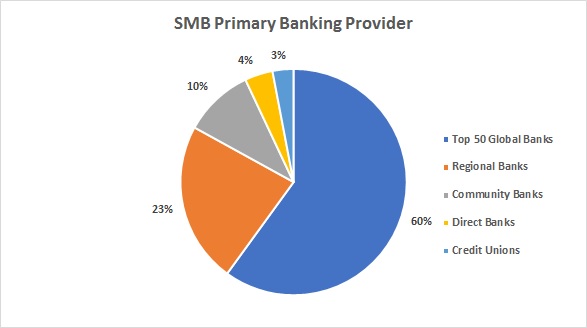

This may spell the most trouble for the top 50 global banks, which the PACE report reveals are the primary banking providers for 60 percent of small and midsized businesses.

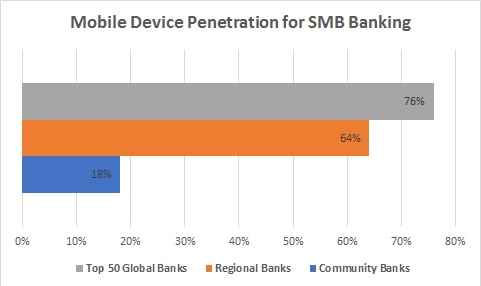

But direct banks, community banks and credit unions are not well positioned, at least at the moment, to win SMB customers from their larger counterparts. The latest PACE report found they are severely behind their larger counterparts in terms of mobile banking penetration.

Clearly, banks of all stripes need to be much farther out in front of the curve to please the digitally-savvy business owners who are driving the bus of the U.S. economy.

The battle is on. Who will win?

You can read the complete 2017 PACE SMB Report, as well as consumer and country specific reports, here.

Anthony Jabbour is the chief operating officer of Banking and Payments for FIS, the world's largest global provider dedicated to financial technology solutions.